We know that contractors with bad credit can still secure emergency capital by leveraging verified purchase orders.

Lenders now focus more upon the creditworthiness of your customers rather than your credit score. These transactional underwriting practices use real-time purchase orders as liquid assets, enabling quick funding for covering material costs without delay.

You may be interested

With the right finance partner and digital verification, you can access funds within 24 hours and maintain operations smoothly.

Exploring this strategy further reveals how it supports long-term growth and financial strength.

Key Takeaways

- Contractors with bad credit can secure emergency capital by leveraging verified purchase orders as collateral instead of relying on credit scores.

- Lenders prioritize customer creditworthiness and purchase order authenticity over contractor past credit, enabling credit-blind funding approvals.

- Digital validation of purchase orders accelerates emergency funding by verifying order status and authenticity in real-time through integrated accounting systems.

- Transactional underwriting uses real-time purchase orders and AI risk assessment to provide instant capital, minimizing default risk for lenders.

- PO financing allows contractors to bridge cash flow gaps without equity dilution, supporting growth and building corporate credit through timely order fulfillment.

The Reality Of Credit-Blind Funding In 2026

In 2026, your FICO score plays a minor role compared with the creditworthiness of your customer when securing funding. We now rely upon transactional underwriting that verifies real-time purchase orders, turning them into reliable collateral. This shift allows contractors access capital quickly by proving current business activity rather than past credit history. Additionally, this model supports subcontractors in unlocking growth capital through their receipts, addressing financial strains. However, many contractors face challenges such as an economic slowdown and workforce shortages, making quick access to capital even more essential for sustaining their operations.

Why Your FICO Score Matters Less Than Your Customer’s Credit

While many contractors worry about their FICO scores, what truly drives funding decisions in 2026 is the creditworthiness among their customers.

Lenders now prioritize a strong customer credit guarantee over the contractor’s past credit, focusing on verified purchase orders as liquid assets. This shift means contractors with bad credit can access capital quickly, as long as their buyers have reliable payment histories.

The customer’s transactional credit signals reduce default risk, enabling credit-blind approvals that authorize contractors to complete projects and secure materials without relying on traditional credit checks. This trend aligns with ongoing workforce and labor challenges, where timely project completion is critical despite worker shortages.

This innovation alters how we approach emergency capital. Our worth is tied to what customers owe us, not our credit past. Embracing this model opens new funding possibilities and fuels growth despite financial scars.

The Rise Of Transactional Underwriting In Trade Finance

Focusing regarding the customer’s creditworthiness changes the entire underwriting game, and transactional underwriting leads the charge. Instead of relying on outdated credit histories, this approach uses real-time purchase orders as clear, verifiable proof of business activity.

That means po financing for bad credit is now a reality. Lenders access directly into accounting systems and procurement portals to confirm the PO’s authenticity and value. This shift eliminates delays and opens emergency capital lines derived from transactional liquidity, not personal credit scores. It also underscores the growing role of AI in finance, particularly in real-time risk management and validation.

With smart escrow handling payments directly to suppliers, risk drops for everyone involved. In 2026, this credit-blind funding revolution enables contractors to release cash quickly, fulfill orders, and rebuild financial strength.

It’s the future regarding trade finance, efficient, transparent, and inclusive.

How Purchase Order Financing Solves The Material Gap

Purchase order financing lets us pay suppliers directly, so projects start at the scheduled time without tying up our own cash. This approach avoids the high costs and risks associated with cash advances, keeping our funds available for labor and other critical expenses. Furthermore, liquidating POs immediately enables contractors to kickstart projects without delays. With the purchase order financing market expected to grow at a compound annual growth rate of 8.7%, this solution is becoming an increasingly viable option for contractors facing cash flow challenges.

Direct Supplier Payments To Accelerate Project Starts

Three key steps define how direct supplier payments through PO financing close the material gap and speed project starts. Initially, the financier verifies the purchase order and approves payment directly to the supplier, bypassing the contractor’s cash constraints.

Secondly, suppliers receive funds via secure wire transfers or certified letters of credit, ensuring materials arrive in a timely manner. Purchase order financing is particularly valuable in construction because it focuses on the supplier’s capability to deliver rather than the purchaser’s creditworthiness. Third, this process allows contractors to meet large orders without relying on traditional credit lines or their own cash.

This method, aligned with purchase order factoring, eliminates delays caused by cash flow shortages and supports rapid project kickoff. By enabling transactional liquidity and supplier enablement, contractors can scale efficiently, bridging material gaps quickly while maintaining financial control and operational momentum in today’s progressing construction environment.

Avoiding The Debt Trap Of High-Interest Cash Advances

While cash advances might seem like a quick fix for bridging material costs, they often come with steep interest rates and hidden fees that can trap contractors in a costly debt cycle.

High-interest rates, sometimes reaching 29%, along with ongoing fees, create debt burdens that grow quickly, making it hard for businesses to stay profitable.

That’s where purchase order financing changes the game. Instead of relying upon personal credit or expensive advances, we use purchase order financing for funding materials directly. This approach covers production costs upfront, pays suppliers for our behalf, and repays with customer payments after project completion. By ensuring timely payment to suppliers, purchase order financing eliminates delays that could otherwise stall project progress.

Preserving Cash Flow For Labor And Operational Overhead

Because material costs often demand substantial upfront cash, obtaining funding that directly covers these expenses lets us keep our internal cash flow focused on labor and operational overhead.

Emergency material funding helps us avoid diverting reserves meant for payroll and site management. This approach guarantees timely supplier payments and fluid jobsite activities.

We maintain liquidity for operational expenses while bridging material procurement gaps with short-term finance, directly paying suppliers. This innovation protects labor continuity and avoids production delays, fitting smoothly into project cycles. CredAble’s quick disbursement process ensures funds are typically received within 4 business days, enabling prompt supplier payments and uninterrupted operations working capital availability.

| Benefit | Impact |

|---|---|

| Direct supplier payments | Preserves contractor cash reserves |

| Labor cost coverage | Sustains workforce during projects |

| Operational overhead funds | Supports uninterrupted site operations |

| Short-term funding | Aligns with project timelines |

| Collateral-free lending | Enables growth without asset pledges |

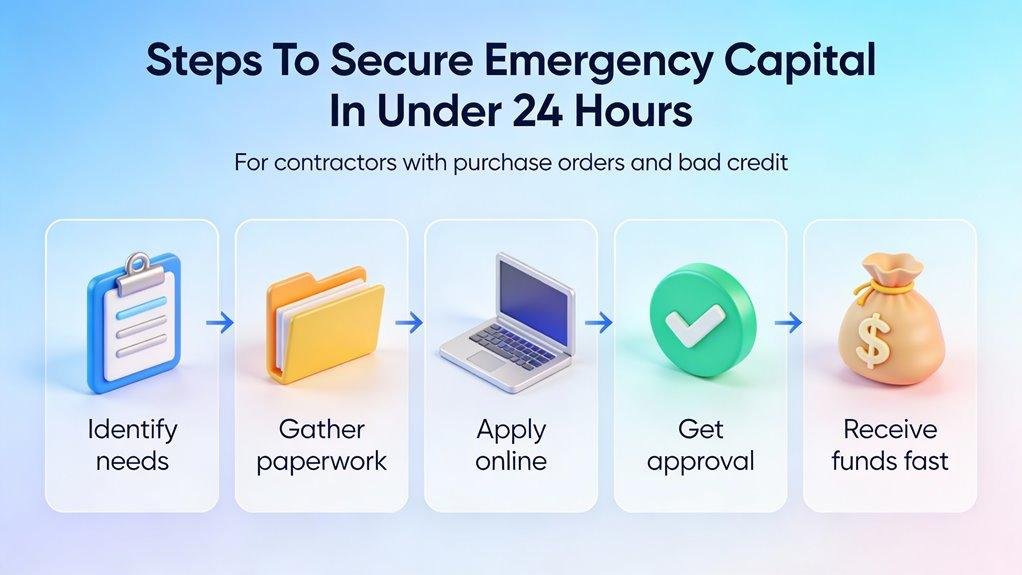

Steps To Secure Emergency Capital In Under 24 Hours

In order to secure emergency capital in under 24 hours, we initially need to validate your purchase order digitally, confirming its authenticity and current status. Next, we select the right 2026 alternative finance partner who uses ledger-based lending to connect directly with your accounting and procurement systems. These steps guarantee swift approval and funding, giving you the transactional liquidity needed to keep your projects moving. This process can also help you access emergency liquidity for operators when critical appliances fail during service.

Validating Your Purchase Order Digitally

As we progress towards securing emergency capital within 24 hours, the initial step is validating your purchase order digitally.

This process begins by defining clear procurement policies that align spending limits with budget controls. We recommend using digital procurement systems that integrate smoothly with your accounting software to streamline approvals and track orders in real time.

Setting up approval workflows guarantees every purchase aligns with company rules, preventing unauthorized spending. Once submitted, the system validates your purchase order against budgets, supplier compliance, and contract terms, flagging any issues before approval.

This rigorous digital validation alters your purchase order into a trusted asset, enabling contractors facing bad credit working capital challenges to tap into swift, reliable emergency funding without traditional credit checks.

Selecting The Right 2026 Alternative Finance Partner

How do we choose the right alternative finance partner in 2026 to secure emergency capital in under 24 hours? It starts by prioritizing speed, flexibility, and integration with supply chain finance 2026 innovations.

We want partners who offer same-day setup, minimal paperwork, and real-time PO verification. Below is a quick comparison to guide our choice:

| Provider | Max Loan Amount | Key Benefit |

|---|---|---|

| Enhancify | $250,000 | Zero dealer fees |

| Wisetack | Varies | Same-day onboarding |

| GreenSky | $65,000 | 0% APR promotions |

Selecting an agile finance partner who supports ledger-based lending enhances our ability to access transactional liquidity quickly and drive supplier enablement without delays or credit barriers.

The Long Term Impact Of PO Financing On Business Growth

When we use PO financing to successfully complete orders, we rebuild our corporate credit by proving our ability to deliver. This approach lets us scale the business without giving up ownership or taking up long-term debt. By relying upon purchase orders as collateral, we keep control while fueling sustainable growth. Additionally, this method often allows construction professionals to tap into funding sources that prioritize performance over credit scores, enhancing our financial opportunities.

Rebuilding Corporate Credit Through Successful Fulfillment

Although poor credit history can limit traditional financing choices, successful use for PO financing lets us rebuild corporate credit by proving our ability in fulfilling orders reliably.

Work-in-progress funding through PO financing bridges cash flow gaps while allowing us to pay suppliers punctually and complete large projects. Each fulfilled order demonstrates operational strength, building a solid payment history that attracts future financing and supplier trust.

This approach moves us beyond old credit metrics, showing financiers what we’re actively doing, not what we did before.

- Regaining control through verified purchase orders as liquid assets

- Strengthening supplier relationships with timely payments

- Building credibility by providing consistent, zero-default performance

Scaling Your Business Without Diluting Ownership

Because traditional financing often demands equity or personal guarantees, many growing contractors hesitate to leverage their business fully. That’s why no-credit-check contractor loans, specifically purchase order (PO) financing, have become a transformative solution.

These loans let us scale without giving up ownership. By capitalizing on verified POs as collateral, we access emergency capital quickly, funding large orders without diluting equity or stressing cash flow.

This transactional liquidity supports supplier payments directly, keeping relationships strong and enabling us to take on bigger projects. Over time, PO financing fuels sustainable growth by improving operational efficiency and positioning our businesses for future opportunities.

We maintain control while expanding, thanks to smart, data-driven lending that values current activity over credit history, putting innovation and long-term success within reach.

Frequently Asked Questions

How Does Smart Escrow Protect Suppliers During PO Financing Transactions?

Smart escrow protects suppliers by securely holding funds until delivery milestones are met, releasing payments automatically following verification, preventing premature release, ensuring timely compensation, and reducing risks—so we all innovate with confidence and avoid costly disputes.

Can Contractors Without Accounting Software Access Ledger-Based Lending?

Yes, we can access ledger-based lending without accounting software by providing financial records like tax returns and bank statements. Lenders value income stability and project history, so we focus at clear, accurate documentation, not software presence.

What Types of Purchase Orders Qualify as Liquid Assets in 2026?

We know 2026 values government and reputable corporate purchase orders as liquid assets—only those fully executed and verified in real-time. Sales orders don’t qualify; this is all about transaction-backed, ledger-verified, PO-backed liquidity driving funding innovation.

How Is Supplier Enablement Measured in Transactional Liquidity Models?

We measure supplier enablement by enrollment rates, time to onboarding, compliance completion, and adoption of digital tools. These metrics guarantee suppliers integrate smoothly, fueling transactional liquidity and enabling contractors with quicker, more efficient procurement and payment cycles.

Are There Risks Associated With Relying Solely on OPC Financing?

Yes, relying solely upon OPC financing carries risks like overexposure to customer credit and potential cash flow disturbances if POs delay. We recommend blending OPC with diverse funding sources for resilience and steady transactional liquidity.